DeFi Lending and Borrowing Guide

The financial world is built on lending and borrowing money. Vast amounts, in fact: there isn’t enough actual cash in the system to repay all of it. But dealing with banks, financial institutions, and middlemen of all stripes is usually a pain. We’ve all been there. The best you can say about them is that they’re better than that 60% APR company always advertising on the cheap TV channels, or that dodgy chap down the road in the sharp suit and the baseball bat.

DeFi (“decentralised finance”) was initially built on an improved version of the blockchain technology that originated in Bitcoin, implemented in Ethereum: a project to realise the vision of a global worldwide virtual computer.

Improved how? The “Blockchain” (a worldwide database/ledger) became smart enough to process financial transactions on its own, running “Smart Contracts”. Things were off and running!

You can read more about it here.

Like most concepts in DeFi, it borrows a lot of concepts and activities from traditional finance, but it’s all done very differently. The most obvious difference is that you’re borrowing, lending, spending and earning crypto, whether it’s stablecoins, proper cryptocurrencies, tokens, or any combination of those.

The other big difference is that DeFi doesn’t know who you are: it’s all anonymous. This means that the lending platforms have to be bullet-proof in enforcing the smart contracts that do the heavy lifting to make sure the system works.

How DeFi Lending Works

The first step is to go to the website of a “protocol” and stake your crypto.

DeFi is very fond of the word “protocol” because they just love technical words, but they really mean a DeFi platform. Three of the biggest are AAVE, Compound and Maker (home of the DAI US dollar stablecoin).

It’s not just interest that you get: with all of those, lenders who stake their crypto receive some of the protocol’s own tokens, kind of like loyalty points. These are still tradable for other cryptocurrencies and stablecoins.

Compound’s token is COMP, Aave generates LEND for you, and Maker issues DAI. COMP and LEND are “Governance tokens”, so they also give you a say in how the platform is run. DAI is a digital dollar.

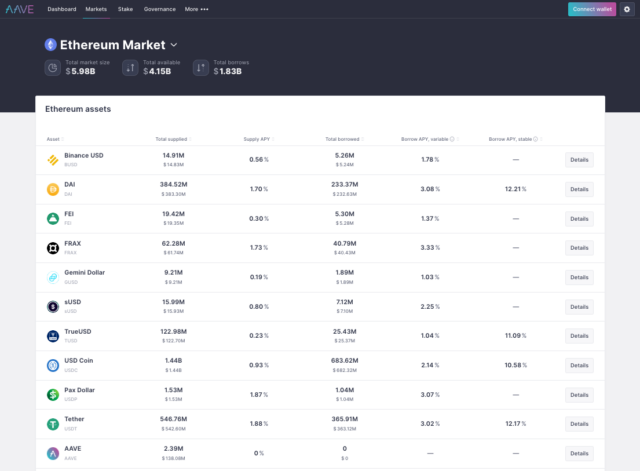

Here’s a snapshot of AAVE’s markets today (17/06/22):

In these post-crash times, you can see the yields are fairly low, but the cost of borrowing is higher. This interest rate difference is what funds interest payments at AQRU.

If you look in the top corner, you can see “connect wallet”. If you have the Ethereum “MetaMask” browser extension, pressing this button will bring it up, and you can log in. Then, the site can see your crypto, and use it. Metamask does ask permission for transactions, btw. It would be scary if it didn’t!

How DeFi Borrowing Works

In the old days, “pawn shops” were common. You would borrow money from a pawn shop, and pay them back with interest. But how did the pawn shop deal with the risk of not being paid back?

The answer is that they’d demand a valuable, saleable item from the borrower to keep until the loan was paid back: this was “collateral”. If the borrower didn’t repay the loan on time, the item was sold and the money was put towards the loan.

Whatever item it was, it needed to be more valuable than the amount borrowed, so that the lender wouldn’t make a loss if he had to sell the item to repay the loan. This means that the loan was “over-collateralised”. The borrower could easily make more money than they needed to borrow just by selling the item, but they wanted to keep it.

Eventually, banks came up with the idea of credit ratings, creditworthiness and credit limits to be able to loan without demanding collateral (though mortgages still require a “charge” over your house – understandable considering the amounts involved). Mortgages are also the main users of the concept of “LTV” – 90% LTV meaning they will only lend you 90% of the value of your house.

The DeFi we’re talking about is anonymous. That means we’re back to collateral, even for small loans.

A borrower has to deposit more crypto than the amount they need, and then digitally sign a loan agreement.

Why would a borrower ever agree to deposit more than they were borrowing? Simple: they don’t want to sell the assets, same as with the pawn shop. It might be more tax-efficient to borrow money against them, too – it’s cashing out without cashing out.

A sting in the tail…

With companies such as AQRU, your capital will always be there. The dollar value of crypto might be less, but the amount of the asset will never go down.

That’s not true with DeFi lending or borrowing. After all, a smart contract can’t force a human to repay a debt. The debt is covered by the collateral of course, so in theory, all is well.

Here’s the sting in the tail: the value of the collateral can change drastically over time, and that can result in the system penalising both the borrower and (sometimes) the lender.

Let’s say that you deposit 1 bitcoin as collateral (when Bitcoin is worth $50,000), and borrow $25,000. That’s a “loan-to-value” of 50% – the loan is worth 50% of the collateral.

Now, let’s say there’s a massive Bitcoin crash and Bitcoin suddenly halves in price. Suddenly, the Bitcoin is worth $25,000 and the loan was $25,000. That’s an LTV of 100%! What happens if the LTV goes over 100%?

It never will. Long before that happens, the system will have stepped in to “liquidate” assets. When does that happen? It depends.

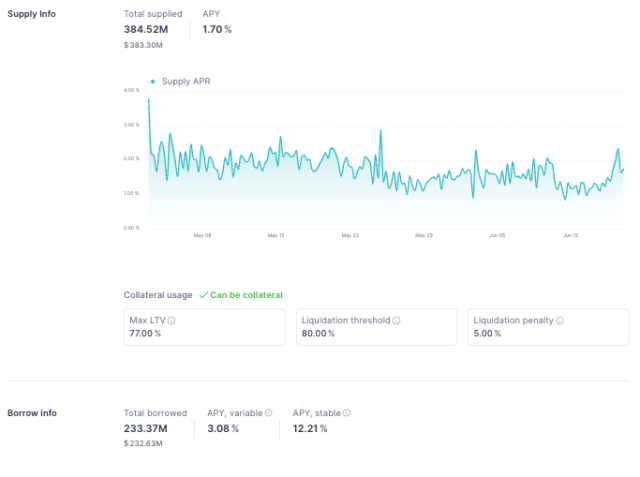

Have a look at this information about borrowing/staking DAI that we captured from AAVE.

What does this tell us?

First of all, it shows us that this is a big market: there’s the equivalent of $385m in the loan supply, of which $233m has already been borrowed. Second, it shows you that the current yield on any deposit is 1.7% APY.

It also tells lenders that borrowers can only borrow up to 77% of the value of their collateral (whatever that is: it doesn’t have to be bitcoin).

We can see from this that there’s a choice of two interest rates for borrowing: 3.03% if you don’t mind the interest rate going up or down over time, or 12.20% if you want it fixed.

The nasty bits are “Liquidation Threshold” and “Liquidation Penalty”.

The “liquidation threshold” is 80%.

That means, if the value of your collateral shrinks so that it’s 80% of the value of the loan, the borrower’s collateral will be “liquidated”.

In this particular platform, that means they’ll sell half of the borrower’s collateral to repay half of the loan to the lender immediately. And (“liquidation penalty”) they’ll keep 2% of the sale price.

This is bad for the lender and the borrower, of course – and isn’t the fault of either one.

Lending without hassle – let AQRU do the worrying!

As you can see, DeFi lending for yield/interest can be done through reputable platforms: but it isn’t risk-free. If the yields are small and the market moves, you could lose out. In addition, of course, your funds are locked into the loan for the length of the loan.

Offering yields that are always competitive with DeFi (whatever it’s doing), but with much less risk, AQRU offers a much safer way for you to earn money from your crypto. It’s not anonymous, but then, that’s for your security too! Sign up, verify, secure your account, deposit funds, invest and watch your funds grow in the hands of experts.